The Partnership’s Regional Economic Snapshot is our comprehensive semi-annual review of economic conditions in the Baltimore, Washington, and Richmond metropolitan statistical areas. The interconnected corridor – home to nearly 10.5 million residents with a GDP of $1.1 trillion – faces complex challenges this year amid federal downsizing, uneven population growth, and a decline in new housing production.

Below, we highlight 5 significant trends for the region.

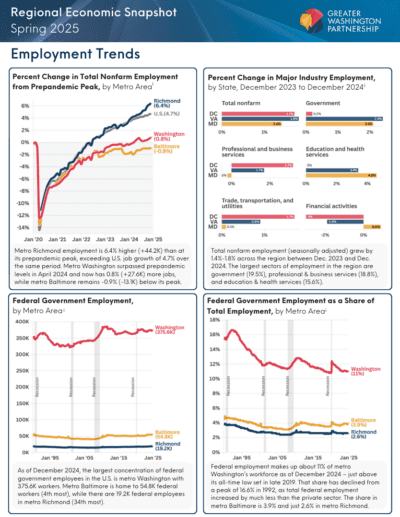

Employment: As a whole, the region recovered from pandemic job losses in early 2024 – but the recovery has been uneven across metro areas.

Since the pandemic, job growth has been strongest in metro Richmond, which is the only part of our region to outpace U.S. job growth over that time. At the end of 2024, employment was 6.4% higher (+44.2K more jobs) than in early 2020.

Metro Washington has been slower to recoup its pandemic-era job losses, finally surpassing that threshold in April 2024. The metro area now has 27.6K more jobs than pre-pandemic – an increase of 0.8%. However, the District of Columbia proper remains nearly 26K jobs below its pre-pandemic employment level.

Metro Baltimore recorded the slowest job growth in the region over the last five years and remains 0.9% below its early 2020 employment level – still down about 13K jobs.

More recently at the state level, total employment grew by 1.4% in Maryland, 1.7% in the District of Columbia, and 1.8% in Virginia in 2024.

Federal Footprint: The regional economy is highly exposed to cuts targeting federal employment and spending, with federal, state, and local government jobs making up the largest industry in the region.

The largest sectors of employment across the District of Columbia, Maryland, and Virginia are government (20% of jobs), professional & business services (19%), and education & health services (16%).

Approximately 11% of metro Washington’s workforce (376K people) is directly employed by the federal government, as of December 2024. Widespread federal layoffs have the potential to significantly affect the local economy, particularly the District of Columbia, where nearly one in four workers is tied to the federal government.

Metro Baltimore is home to 54.8K federal workers, the 4th highest amount among metro areas nationally, making up just under 4% of the area’s workforce. Metro Richmond is much less exposed to potential federal cuts with just 19.2K federal employees, making up 2.6% of the area’s workforce.

The District of Columbia was the largest recipient of federal R&D funding in FY 2022, while Maryland was 3rd and Virginia 4th. Altogether, the three jurisdictions received over $64.3B (about one-third of all federal R&D spending that year), with $16.2B of that amount directed to businesses, higher education institutions, and nonprofits in the region, while $48.1B went directly to federal agencies.

GDP: Over the past five years, economic growth in our region has been stronger than other large metro areas like New York City, Los Angeles, and Chicago, but it has trailed behind the fast-growing economies of the South and West.

Total economic output across the region neared $1.1 trillion in 2023, with just under two-thirds generated in the Washington metro area.

The combined region of metro Baltimore, Washington, and Richmond has the 4th largest GDP in the country – trailing only metro New York City, Los Angeles, and the Bay Area (San Francisco + San Jose). Independently, DC ranks 6th, Baltimore 19th, and Richmond 43rd.

Combined, the region’s three metro areas grew at an annualized rate of 1.8% in real terms over the past five years, trailing behind the large, fast-growing economies of the South and West but outperforming New York City, Los Angeles, and Chicago.

At the state level, Virginia’s economy has led the region, growing by 3.3% in Q3 2024 relative to the same quarter a year earlier. Economic growth in Maryland and the District of Columbia has largely trailed the U.S. over the past few years, coming in at 2% and 1.8%, respectively, in Q3 2024.

Population growth: Fewer people moved away from the region in 2024, boosting state-level population growth. Even so, the region remains highly reliant on immigrants for its growth.

Immigration remains the largest source of population growth across all three jurisdictions – particularly Maryland, which would have lost population in 2024 without international transplants.

Virginia added 76.5K residents, growing 0.9% to 8.8 million people between July 2023 and July 2024. Domestic migration swung positive last year, making it the only regional jurisdiction to see more people move in from other states than move away (+5.3K).

Maryland’s population ticked up to 6.3 million in 2024 – an increase of 46.2K (0.7%) from the year prior. Without international migrants (53.1K), population would have declined due to significant domestic migration to other states (-18.5K).

The District of Columbia added nearly 15K residents last year, surpassing 702K and growing 2.2% – faster than any state in the country. However, the District remains heavily reliant on international migrants for almost all its growth.

Housing:New housing permit approvals declined across the region in 2024, even as affordability remains a top concern.

Relative to the size of its population, metro Richmond is the region’s leader in housing production, permitting 6.4 new units per 1,000 residents in 2024 – faster than the country overall and on par with rapidly growing Atlanta.

Metro Washington approved building permits for 21.9K units in 2024, a significant drop from 2022 and less than its typical pre-pandemic levels. On a per capita basis, metro Washington surpasses other large legacy metros with 3.5 units permitted per capita.

Baltimore’s rate of production was the region’s lowest at 2.2 units per capita, as it contends with sluggish population growth and a surplus of vacant and abandoned housing units in Baltimore City.

Download Report »

Download Report »